By Paul Mullins OBE, Non-Executive Chairman, Aptem

GDP is sharply down, and unemployment is rising following Covid-19. Big sectors which have helped many enter the labour force such as hospitality are hard hit and not likely to perform the same role in the next recovery.

How bad could post Covid-19 unemployment become, and what can we do to arrest its growth and help the out of work redeploy their skills? In this piece we look at the ONS forecasts, comparing them with previous recessions and recoveries. We seek to draw conclusions relevant to skills training.

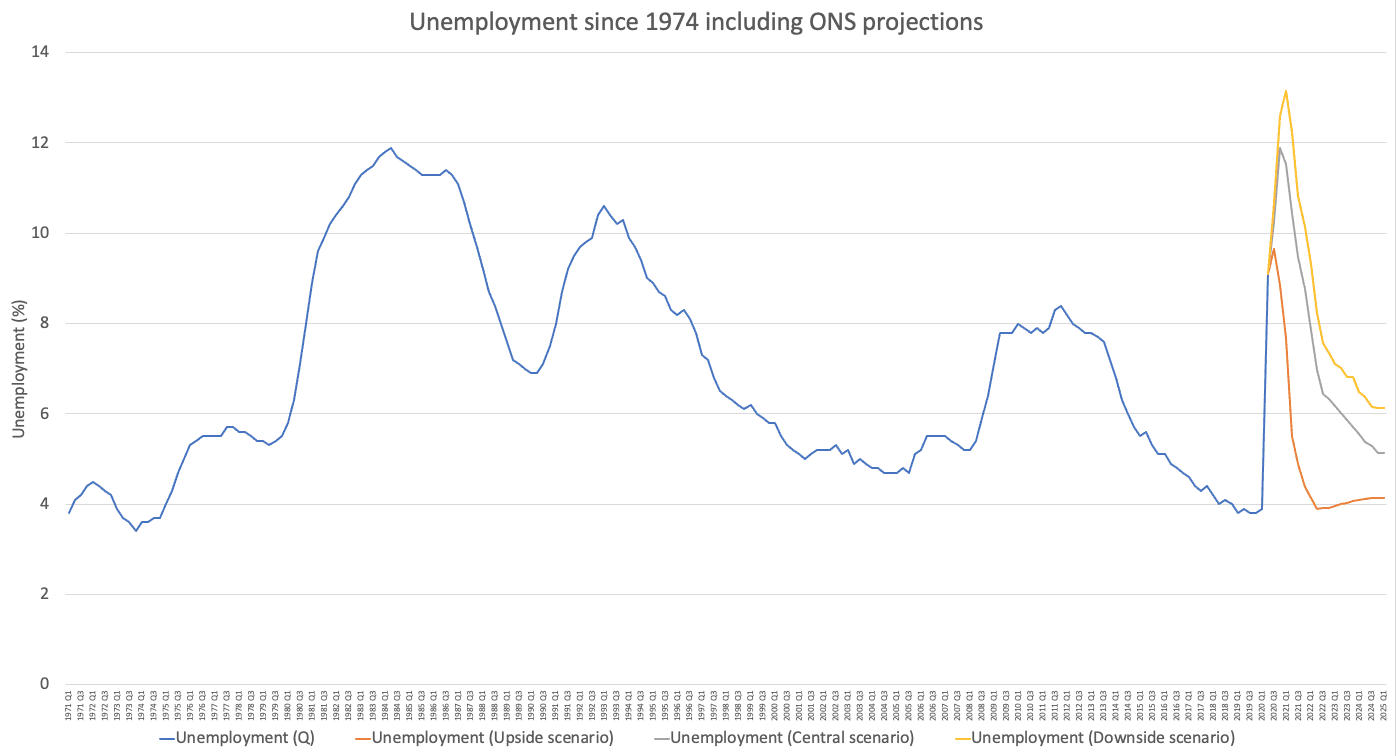

The ONS forecasts unemployment will peak early in 2021 at 13.1 % (worse case) and by Q1 2025 will be 4.1% (best case) to 6.1% (worst case).

Best case scenario

The best ONS case takes us back by 2025 to the immediately pre-COVID level of 3.9%. That is, a sharp rise and a rapid fall.

Looking at previous recessions can help us understand how the COVID-19 unemployment recovery may take shape. It’ll show the feasibility of achieving the rapid fall we would all like to see. They are, of course, precedents and not forecasts.

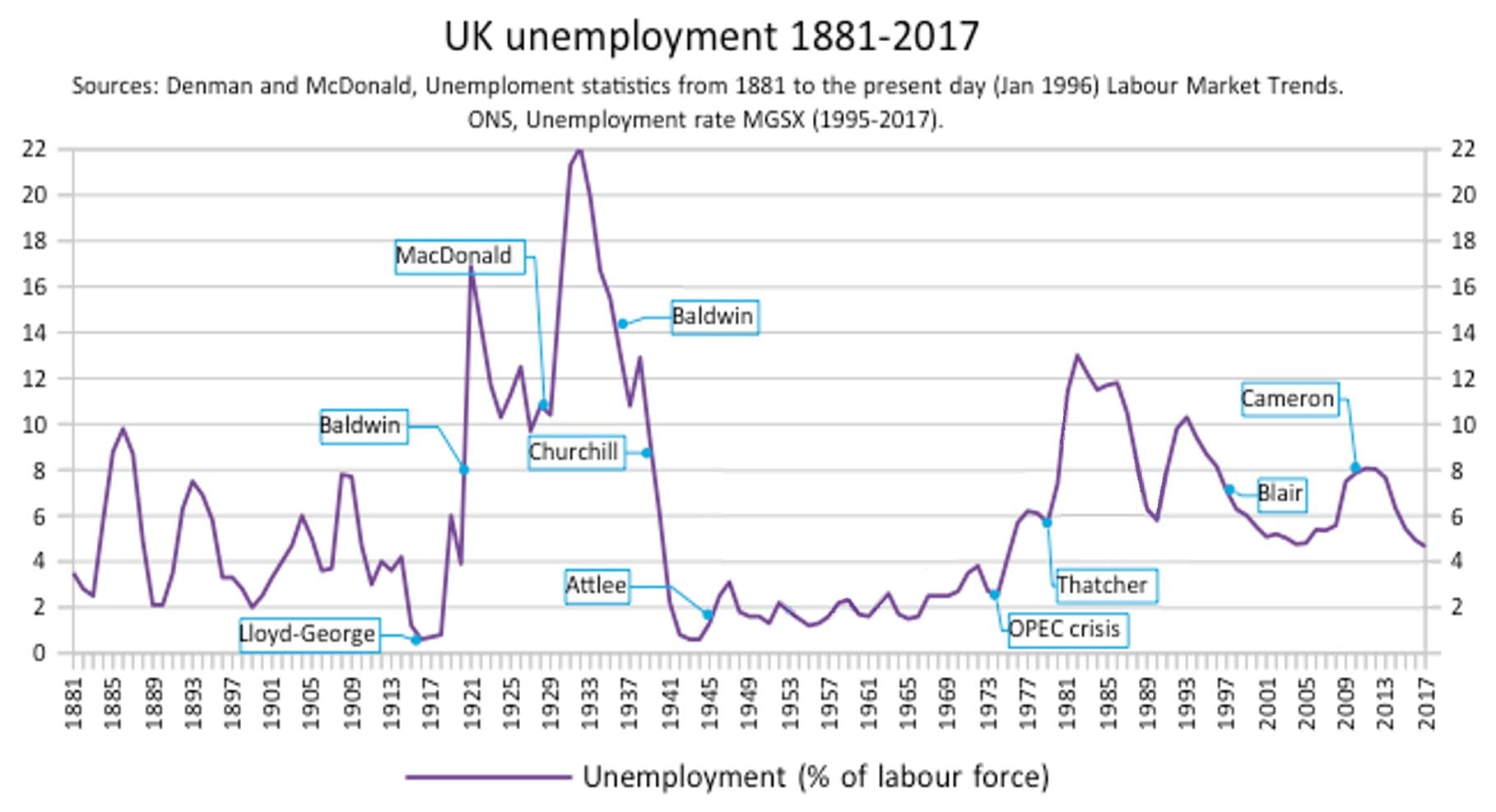

The graph below shows UK unemployment over the last 150 years. In scale, we are likely to be facing unemployment comparable to the early 1980s (12.0%) or even the 1930s with its peak of over 20.0%.

Another global pandemic, the Spanish flu in 1918, coincided with the end of World War One. The two together saw unemployment rise fast from effectively full employment in 1918 to 17% in 1919 and a rapid decline to 10 % by the mid 1920s.

Recent recession data

The 1990 and 2008 recessions are potentially instructive. They are the most recent, have a similar shape to each other and not dissimilar scale.

Let’s analyse the 1990 and 2008 recessions in more detail:

1990

- Q1 1990 unemployment rise from 6.9% to Q1 1993 10.6% – up 54% – in 3.25 years, or 16.6% pa

- Decline from Q1 1993 unemployment of 10.6% to 1997 Q3 6.9% – previous level – down 36% in 4.5 years, or 8.0% pa

- Decline from Q1 1993 unemployment of 10.6% to Q1 2004 4.7% – new low – down 56% in 11.0 years or 5.1% pa

2008

- Q1 2008 unemployment rise from 5.1% to Q3 2011 7.9% – up 55% – in 3.5 years, or 15.7% pa

- Decline from Q3 2011 unemployment of 7.9% to Q4 2015 5.1% – previous level – down 35% in 4.5 years, or 7.83% pa

- Decline from Q3 2011 unemployment of 7.9% to Q2 2019 3.8% – new low – down 52% in 7.75 years or 6.7% pa

The conclusions, based purely on these two recessions, are that:

- Unemployment rises at ~16% pa for three years.

- It falls ~8% pa to its previous pre-recession level over a period of 4.5 years.

- Falls to that previous level take 1.2 to 1.4 times longer than the rises.

- It falls at 5-7% pa to new lows over a period of 8-11 years.

- Falls to those new lows take 2.2 times to 3.5 times longer than the rises.

What might happen now?

Based on those past recessions, unemployment would rise by 16.0% every year or from 3.9% to 6% between 2020 and 2023. And then decline back to its previous level over a period of 4.5 years to 2028.

All recessions have unique characteristics, and 2020 feels – and is already forecast to be – much more extreme. A recession is defined as at least two successive quarters of negative GDP growth. In 1990, the decline was around 2.0 per cent and in 2008 a little over 5.0 %. In 2020 it has exceeded 20%.

What is the skills need behind the forecasts?

The ONS is forecasting a much quicker steeper rise in unemployment. A decline taking us back to 3.9% by early 2025 is very fast. How could this come about?

The ONS has made forecasts of unemployment by sector according to the impact of the Covid response and restrictions. In July 2020 58% of jobs in the Accommodation & food services sectors were furloughed, along with 36% in the Arts, entertainment, recreation and other services sector, and 32% in the Wholesale and Retail sector. The latest data shows that vacancies in these sectors have reduced year-on-year by 72%, 82% and 61% respectively compared to an average decrease of vacancies 46% across all sectors. Comparing these three service sectors to other sectors, there is likely to be a far greater number of redundancies and reduced demand for jobs.

There are three major trends:

- large-scale switches of sector

- support to help unprecedentedly large numbers find new work

- a huge volume of support to help people gain the skills required to do different work.

We have no living experience of large parts of the economy shutting down and potentially not recovering. Hospitality, travel, and retail to name three are hamstrung by the continuing need for distancing – and, as time goes on, social patterns changing for the long term.

Switching sectors

Planning rapidly to reabsorb large numbers into work will necessarily involve large sector switches.

There is a powerful economic driver for government to speed the process of finding new work as much as it can so help with outplacement, identifying existing skill strengths and presenting them to potential employers will all be needed in scale.

Many of the worst affected sectors are relatively low-skilled. Getting people back into employment means they switch to sectors requiring more skills. Our challenge and also our biggest opportunity is to transform skills and lift large numbers out of low-waged, low-skilled work, tackling unemployment and raising productivity.

Successful sector switching will involve significant retraining and upskilling

The strong need for skills training

If our analysis is correct, we have a strong signal of the demand that is going to be placed on the whole skills training sector. It is good too in that it coincides with that longstanding national need to raise productivity. An unprecedently large proportion of the working population has an unsought and unwelcome change of employment coming. Many of the sectors that have recently supported job creation are relatively low – skilled and low wage. As they are also amongst the hardest hit by the pandemic we need to make that a big upskilling programme too. Let’s make sure we tackle unemployment and productivity helping people find new jobs that are higher skilled and more rewarding.

Financial pressures are big

That COVID puts pressures on public finances is understood. Furlough has been estimated by the ONS to cost £14 billion a month, adding to the pressure the public finances were already under.

The OBR measure of Public Sector Net Debt as a percentage of GDP has more than doubled from 2008 when it was around 30 .0 % of GDP to over 60.0 % by 2011 and went on climbing. It had not fallen below 70.0% pre-COVID and is now rising sharply again. This is far above the long-term trend of 20.0% to 50.0%.

Faced with competing priorities at a time of such unprecedented challenge government takes heed of those who cogently present solutions to problems that are practical not theoretical and are ready to go.

Funding for training has to make its case to compete for scarce government resources

Skills training: up to the challenge

For everyone involved in skills training, the situation is uncertain – but it is tending to positive. Nationally we face a generational challenge. Skills training is one of the most important ways we have to meet the challenges of high unemployment and low productivity.

Skills training – apprenticeships, study programmes and AEB – are key parts of a strong, growing system, pre-wired to address the three big goals:

- Engaging and incentivising employers to take on employees with fresh relevant skills

- Supporting employers in shifting to new business models needing new skills

- Supporting employees changing sectors and roles

One key reason why this comes about will be the skills training sector – individually and together – confidently asserting the vital role it is ready to perform.

The challenge is to be ready to make this post-COVID-19 unemployment re-training robust and in scale to meet demand.

Post-COVID training

Training delivery is for the future only robust if it is delivered online. High quality distance learning was always needed and is now essential. Leading providers describe it as the silver lining to the dark COVID cloud, realising the benefit of fit-for-purpose systems to be online, efficient, and robust. This does not replace face-to-face teaching, but it helps reserve that for the most valuable of interactions and ensures that everyone can carry on if lockdowns return.

How Aptem helps

Our systems support end-to-end delivery. Our award-winning platform is trusted by training providers, universities, colleges, employer providers and thousands of users across the UK.

We have four skills training systems on the Aptem platform:

Award-winning platform trusted by training providers, universities, colleges and employer providers.

Enables you to quickly deliver quality training online. Integrated Zoom training ensures business continuity through these challenging times.

End-to-end platform that delivers fully compliant AEB training combined with employability resources to ensure rapid re-employment, supporting classroom, blended delivery and distance learning. Winner of several industry awards.

Helping FE Colleges and private training providers deliver and evidence the employability components of Study Programmes. It delivers employability training, supports work experience and provides job finding resources.

An award-winning solution to support providers to place high volumes of job seekers back into work, quickly and for the long-term. Combines powerful case management with self-service jobseeker portal.

Let’s talk

We know that skills teaching across the board has many new challenges. We are supporting over 100 clients with tens of thousands of learners live on our platform today. Since the pandemic arrived, we have been spending much of our time talking to existing clients and to those joining us each month about the distinct shape of their challenge and how what we do can be a useful part of their response. We don’t do software in a box. We supply systems, service and solutions.

The problems we face are national and huge in scope. The solutions are much more individual. We can all drive what we do now to have the greatest impact – and to have the greatest influence over what government does too.

If you would like to talk about meeting your challenges please get in contact.